February 20, 2026

Contribution Margin-Based Pricing

Contribution margin-based pricing is a strategy where businesses set product prices by first accounting for variable costs and then ensuring each sale contributes toward fixed costs and profit. It gives retailers a clear view of how much revenue each unit generates beyond its direct production cost

Drishti, Manager - Digital Marketing

Table of Contents

- What is Contribution Margin-Based Pricing?

- How to Calculate Contribution Margin?

- What are the Benefits of Contribution Margin-Based Pricing?

- What is the Difference Between Contribution Margin and Gross Margin?

- How to Set Prices Using Contribution Margin?

- When Should Companies Use Contribution Margin-Based Pricing?

- Optimize Your Contribution Margin-Based Pricing Strategy with Flipkart Commerce Cloud

Contribution Margin-Based Pricing

Retailers constantly seek efficient methods to balance competitive rates with necessary profitability levels. Contribution margin-based pricing is a vital financial tool for understanding the direct profitability of individual items in inventory.

This approach moves beyond simple revenue tracking by isolating variable costs directly tied to sales volume. Companies utilize contribution margin-based pricing to determine which products truly support the broader cost structure and long-term goals.

- It allows businesses to identify exactly how much money remains after covering the direct production and shipping expenses involved, ultimately generating profit.

- The method helps managers make informed business decisions regarding product discontinuation or promotional strategies for their current active inventory.

- Retail owners gain clarity on how pricing adjustments impact the overall financial performance of their specific retail operations.

- Contribution margin-based pricing provides a clear framework for establishing break-even points across different product categories effectively and accurately.

What is Contribution Margin-Based Pricing?

Contribution margin-based pricing is a strategy where you set the price of a product to cover variable costs first, then contribute to fixed costs. You use this method to ensure that each unit sold covers its own production costs and benefits the business.

It focuses on the portion of sales remaining after you deduct the variable costs of producing an item. Retailers relying on contribution margin analysis gain a clearer picture of financial efficiency than those who look only at sales revenue or sales volume. It provides valuable insights into the profitability of individual products.

How to Calculate Contribution Margin? (+ Example)

You need to understand the fundamental components of revenue and business costs to apply this contribution margin calculation effectively in your retail business.

In simple terms, the basic formula for contribution margin-based pricing is:

Contribution Margin = Selling Price - Variable Costs

Here,

- Selling Price: The amount the customer pays for one unit of the product.

- Variable Costs: Costs that change with production volume, such as raw materials, packaging, direct labor, and even sales commissions.

- Contribution Margin: The amount left after deducting variable costs from the selling price. This is your dollar contribution toward fixed costs.

To find the contribution margin ratio, you must divide the contribution margin by the sales price.

Let’s consider an example of a beverage company here. Start by determining your unit selling price. Subtract variable expenses such as labor and materials from that figure. For example, selling a craft soda keg for $500 with $300 variable costs yields a $200 contribution margin.

In this case, the contribution margin ratio is (200/500) = 0.40 or 40%.

This means 40% of every sale goes toward covering fixed costs such as warehouse rent, staff salaries, and customer support software subscriptions. Once fixed costs are fully covered, the remaining contribution generates net profit. Multiplying this ratio by your total sales revenue gives you a fantastic high-level view of your earnings potential.

What are the Benefits of Contribution Margin-Based Pricing?

Implementing contribution margin-based pricing offers distinct advantages for retailers aiming to optimize their inventory management and financial planning.

- Break-Even Analysis: It helps companies calculate exactly what number of units they must sell to cover total costs. You can determine the precise volume required to reach zero profit and avoid losses. This insight enables safer expansion plans and more realistic targets for your sales teams.

- Profit Planning: Managers can easily see how changes in total sales affect the total profit. You gain the ability to forecast how a 10% increase in sales affects your profit margin. This helps set achievable quarterly goals while maintaining tight cost control.

- Product Performance: It identifies which products generate the most cash to support the business. You can distinguish between high-volume items with low margins and low-volume items with a higher contribution margin. This clarity helps you adjust your product mix to focus on items with the highest profit potential.

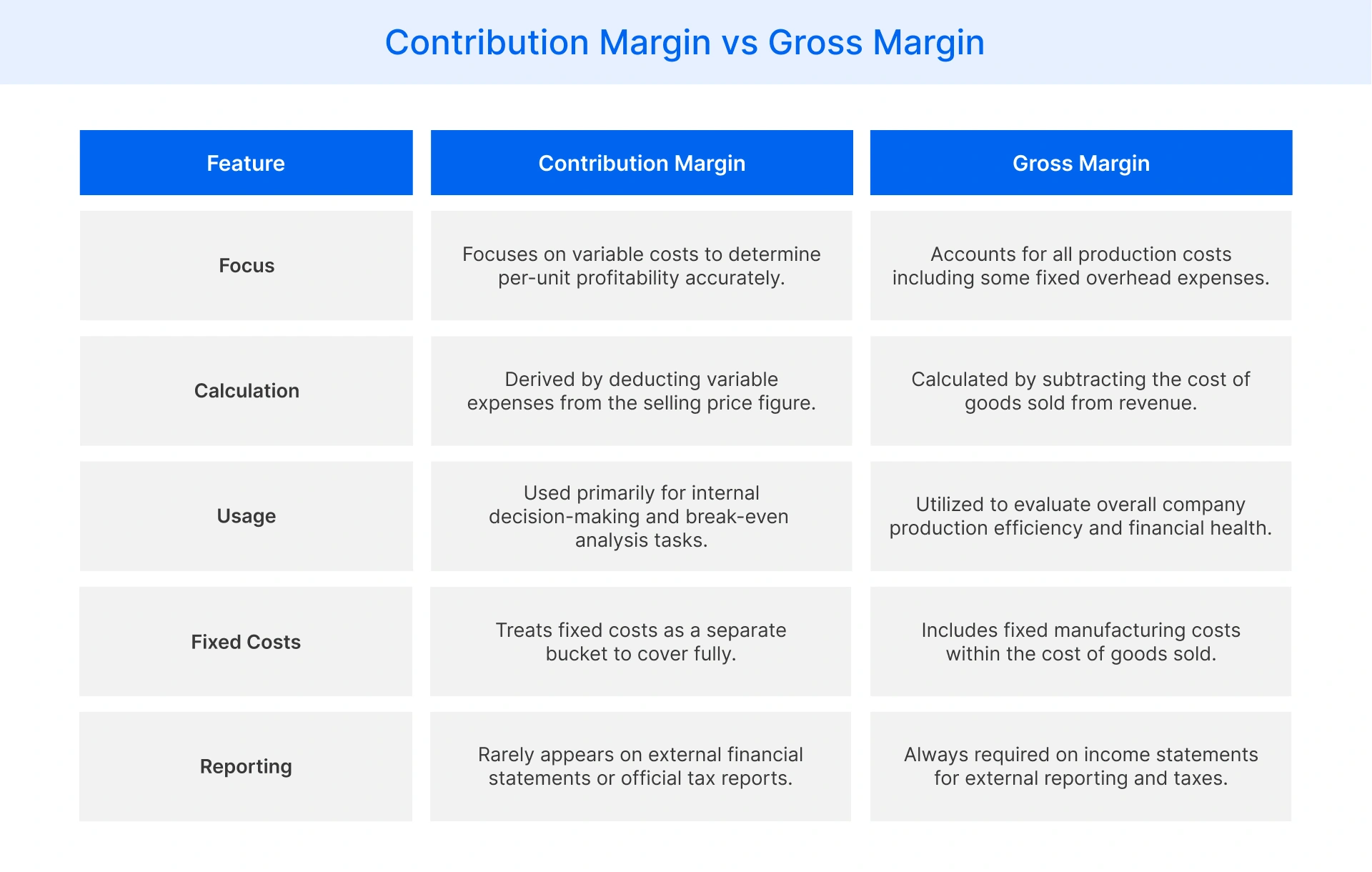

What is the Difference Between Contribution Margin and Gross Margin?

Many retailers confuse these terms, but they serve different purposes. Gross margin includes all costs of goods sold, while contribution margin-based pricing focuses strictly on variable costs. You use the former to assess overall profitability, and the latter to analyze per-unit efficiency and break-even points for specific products.

How to Set Prices Using Contribution Margin?

You can establish a robust contribution margin-based pricing structure by following a systematic approach that prioritizes covering your variable expenses first.

- First, identify the variable cost per unit, including raw materials, direct labor, packaging and any cost that changes based on production volume.

- Next, determine the contribution margin amount you need to cover your fixed overheads, which typically includes costs like rent, utilities and administrative salaries.

- Then, add the desired contribution margin amount to the variable cost per unit to arrive at a baseline price that meets your financial targets.

- The resulting total is your target selling price, which ensures every unit sold actively supports cost recovery and contributes to overall profitability.

When Should Companies Use Contribution Margin-Based Pricing?

Retailers encounter scenarios in which this pricing model outperforms others by securing essential cash flow for daily business operations.

- New Product Launch: You can use contribution margin-based pricing to set a low introductory price that covers variable costs while attracting early customers. This strategy minimizes risk during market entry by ensuring you do not lose money on each unit sold to new buyers.

- Slow Seasons: You may use this method to lower prices temporarily during off-peak times to keep operations running without losing money. Covering variable costs during slow periods ensures you maintain cash flow even if you are not covering the full fixed overheads.

- Discontinuing Products: This metric helps you decide if a low-performing product is worth keeping or if it simply drains your resources. You can see if an item covers its own variable costs or if you should remove it to free up capital.

Optimize Your Contribution Margin-Based Pricing Strategy with Flipkart Commerce Cloud

Effective pricing requires you to see beyond simple costs. You need to understand how every price change impacts your contribution margin-based pricing strategy and overall profitability across your entire catalog. We help you visualize these complex data points clearly.

Flipkart Commerce Cloud lets you automate this complex analysis. We provide the tools you need to track variable costs and adjust prices dynamically in real-time. Our system ensures you react instantly to market fluctuations or cost changes.

FCC Pricing Manager integrates margin data with competitor insights to ensure every price you set contributes to your bottom line. You can secure your profits while staying competitive in the market. We empower you to make data-driven decisions that scale.

Take control of your margins today. Explore our solutions and start pricing with confidence.

FAQ

No, they are distinct financial concepts. Profit is what remains after you subtract all fixed and variable costs from revenue. In contrast, contribution margin-based pricing only accounts for variable costs. You use the latter to understand how much cash a product contributes toward paying off fixed expenses like rent.

Yes, this can happen if your variable costs exceed the selling price. A negative margin means you lose money on every unit sold before even paying fixed costs. You must adjust your contribution margin-based pricing immediately or discontinue the product to prevent significant financial damage to your retail business.

It clarifies which products actually support your business. You can decide which items to promote, which to discount, and which to drop. By focusing on contribution, you ensure that marketing dollars go toward high-return items rather than products that barely cover their own production costs or shipping fees.

Variable costs are expenses that change in direct proportion to production volume. These typically include raw materials, direct labor, packaging, and shipping fees. You must track these accurately because they are the primary deduction in the calculation used to determine the efficiency of your individual product pricing strategies.

It is the core component of the break-even formula. You divide your total fixed costs by the contribution margin per unit to find the break-even point. This tells you exactly how many units you need to sell to cover all expenses, ensuring your business stays financially solvent and secure.