December 19, 2024

Absorption Costing

Absorption costing is an accounting method used for capturing all costs related to making a product, including materials, labor, rent, and insurance.

Drishti, Manager - Digital Marketing

Table of Contents

- What is absorption costing?

- What is the absorption costing calculation?

- What are the components of absorption costing?

- What is an absorption costing example?

- Advantages of absorption costing

- Disadvantages of absorption costing

- Absorption costing vs variable costing

- Conclusion

What is absorption costing?

Absorption costing, also referred to as full costing, is a pricing strategy that includes both variable and fixed costs related to the production of a specific unit of a product. Like many other strategies, the primary objective of absorption pricing is to determine the optimal cost that ensures a substantial profit margin.

The composition of fixed and variable costs typically includes expenses related to materials, labor, rent, and insurance. The combination of these costs facilitates the determination of an appropriate price that ensures an optimal profit margin. When it comes to absorption pricing, the integration of variable costs with fixed costs is extremely important.

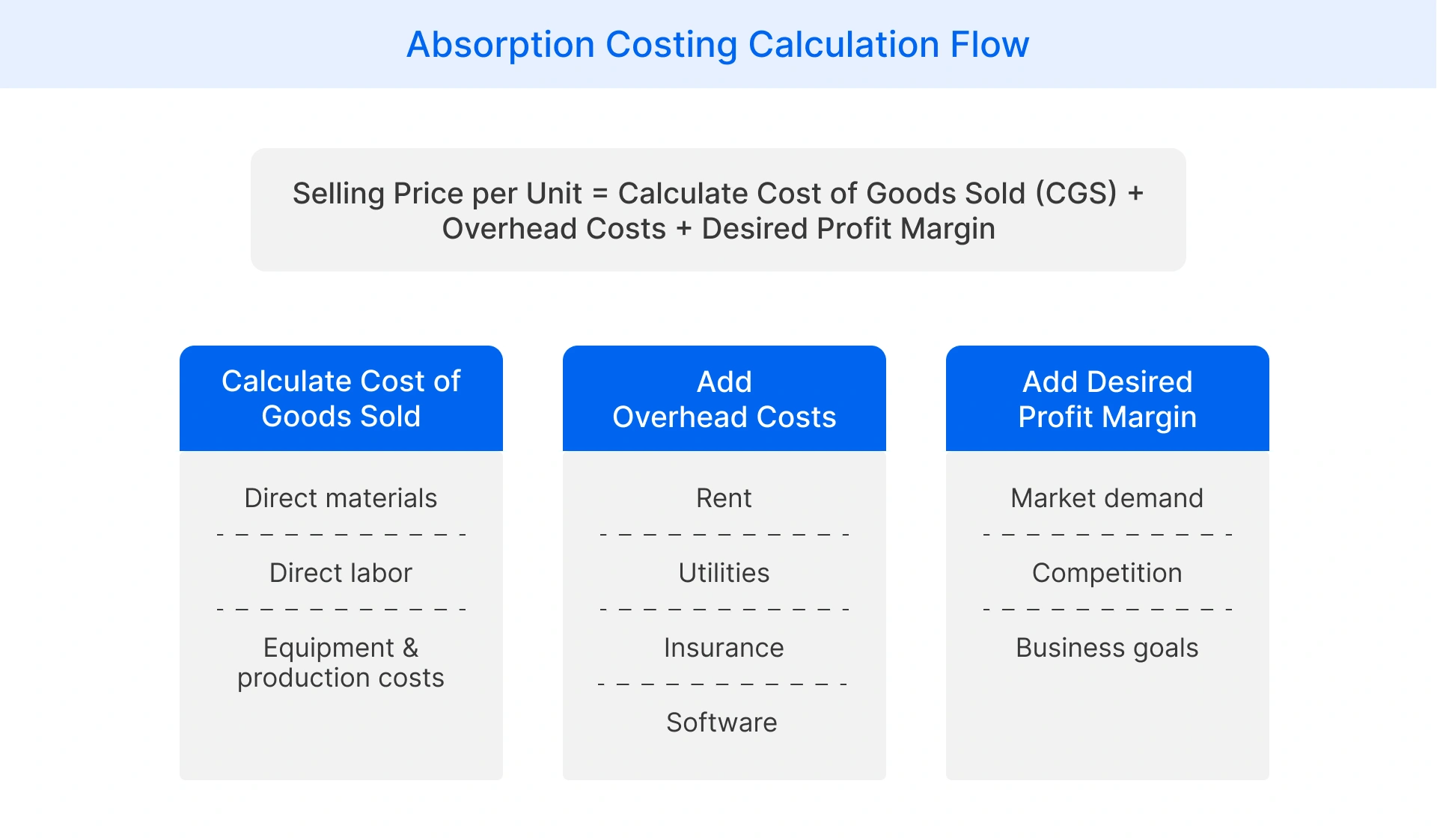

What is the absorption costing calculation?

To determine absorption costing, a retailer must first understand both variable and fixed costs. The calculation process involves several key steps:

Calculate the Cost Price: Begin by determining the Cost of Goods Sold (COGS), which includes direct costs like product acquisition, raw materials, labor, and equipment. Then, add overhead costs such as rent, utilities, insurance, and software.

Add the Profit Margin: Once the cost price is calculated, add the desired profit margin. This margin should be based on factors like market demand, competition, and the retailer's financial goals.

By following these steps, a retailer can set a reasonable price for each unit that covers all costs and generates a desired profit.

What are the components of absorption costing?

Absorption costing is a cost accounting method that allocates all manufacturing costs, both direct and indirect, to products.

Direct Costs: These are expenses directly attributable to a specific product or service. Examples include raw materials, labor, and any other costs incurred during the production process.

Indirect Costs (Overhead):These variable overhead costs cannot be directly traced to a particular product. They are allocated to products based on a specific activity measure, such as direct labor hours or machine hours. Examples include rent, utilities, and insurance.

In absorption costing, both direct and indirect costs are factored into the cost of each unit of a product. The total manufacturing costs are then divided by the number of units produced to determine the cost of each unit.

The formula for absorption costing is:

|

Absorption cost = (Direct Labor Expenses + Direct Material Costs + Variable Manufacturing Overhead Expenses + Fixed Manufacturing Overhead Costs) / Number of Units Produced |

What is an absorption costing example?

Here’s an example of absorption costing:

ABC Enterprises produces a range of electronic gadgets in its manufacturing facility. In February, it produced 15,000 gadgets, of which 12,000 were sold by the end of the month, leaving 3,000 still in inventory.

Each gadget uses $6 of labor and materials directly attributable to the item. Additionally, there are $30,000 of fixed overhead costs each month associated with the production facility.

Under the absorption costing method, the company will assign an additional $2 to each gadget for fixed overhead costs ($30,000 total ÷ 15,000 gadgets produced in the month).

The absorption cost per unit is $8 ($6 labor and materials + $2 fixed overhead costs).

As 12,000 gadgets were sold, the total cost of goods sold is $96,000 ($8 total cost per unit × 12,000 gadgets sold).

The ending inventory will include $24,000 worth of gadgets ($8 total cost per unit × 3,000 gadgets still in ending inventory).

Advantages of absorption costing

- Simplicity: The main advantage of absorption costing is that this method is relatively easy to understand and implement, making it a suitable method for most retailers.

- Profit Assurance: By allocating both fixed and variable costs to products, full absorption costing provides a clear picture of a product's full cost. This helps set prices that cover all costs and ensure the company's profitability.

- Ease of Formulation: The calculation process for absorption costing is simple. This makes it relatively easy to determine product costs and pricing.

- Transparent View of Profit and Cost: Absorption costing provides a clear understanding of the profit margin and cost per unit. This allows retailers to make informed decisions about pricing, production, and inventory management.

Disadvantages of absorption costing

The following challenges of absorption pricing highlight that while the strategy might be simple to implement, it is not a one-size-fits-all solution.

- Lack of Competitive Consideration: This method does not consider the pricing strategies of competitors, which can pose challenges.

- Value Aspect Ignored: The approach overlooks the aspect of value. Ultimately, absorption pricing can result in aggressive pricing, prompting your customers to seek alternatives.

- Ease of Formulation: The calculation process for absorption costing is simple. This makes it relatively easy to determine product costs and pricing.

- Potential for Error: The strategy leaves room for error. The formula for absorption pricing incorporates variable and fixed costs, which are derived from budget estimates. Incorrect cost calculations can introduce a margin of error in the entire pricing strategy.

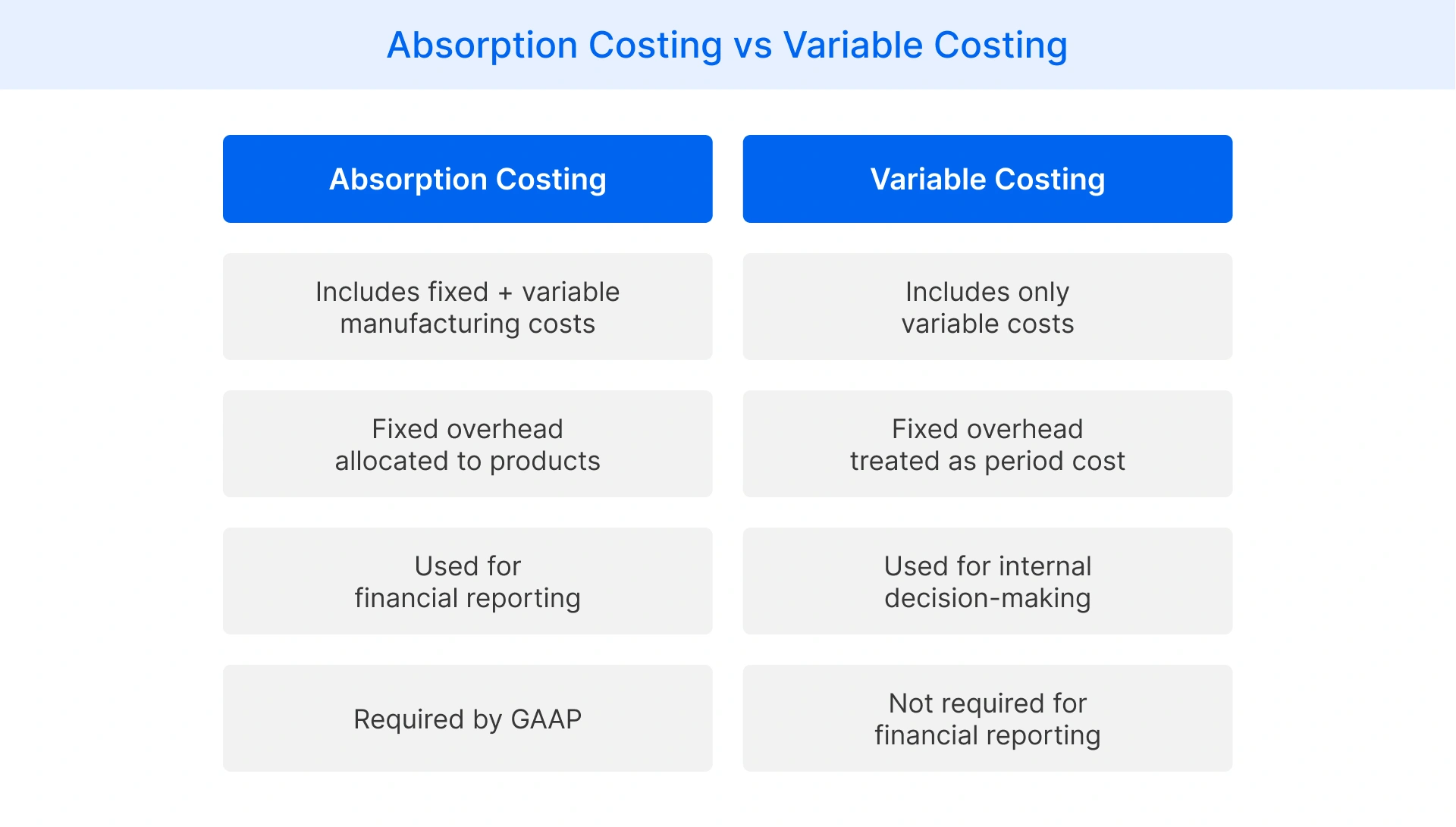

Absorption costing vs variable costing

Absorption costing and variable costing are two distinct methods used to calculate product costs. They primarily differ in their treatment of fixed overhead costs.

Under absorption costing, all manufacturing costs, including direct costs (like raw materials and labor) and indirect costs (overhead), are allocated to products. This method is commonly used for external reporting, such as financial statements.

In contrast, variable costing includes only direct costs in product costs. Overhead expenses are treated as period costs, recorded in the income statement when incurred. This approach is more suitable for internal management decisions, as it isolates variable costs, which are relevant for short-term decision-making.

A key difference between absorption costing and variable costing is the treatment of fixed overhead. Absorption costing allocates fixed overhead to products, resulting in a per-unit cost. Variable costing, however, treats fixed overhead as a period expense, leading to a lump-sum entry on the income statement.

Conclusion

Absorption costing is a comprehensive method that allocates all manufacturing costs, both fixed and variable, to the cost of a product. This approach is essential for determining the cost of goods sold, ending inventory, and profit margins.

Fixed manufacturing overhead costs, while not directly traceable to specific products, are allocated to each unit based on a predetermined overhead rate. This rate is calculated by dividing estimated fixed overhead by expected production units.

By including both fixed and variable manufacturing costs, absorption costing provides a more complete view of a product's cost, which is crucial for financial reporting and pricing decisions.

FAQ

The difference between absorption costing and direct costing involves the specific treatment of fixed manufacturing overhead expenses. Absorption costing includes fixed overhead as part of the product cost and carries it in inventory until the item is sold, while direct costing treats them as period expenses that are fully deducted in the month it occurs. FCC allows managers to toggle between these views to better analyze short-term versus long-term profitability.

Absorption costing means a method of accounting that allocates all manufacturing costs, both direct and indirect, to each unit produced. Also called full costing, it covers direct materials, direct labor, variable overhead, and fixed overhead. This gives businesses a complete and accurate picture of production costs for both pricing decisions and external financial reporting.

The formula for absorption cost is: Direct Labor + Direct Materials + Variable Manufacturing Overhead + Fixed Manufacturing Overhead, divided by the number of units produced. This per-unit figure ensures every product carries its fair share of total production costs. Flipkart Commerce Cloud helps businesses automate this calculation accurately across large and varied product catalogs.

Real world examples of absorption costing appear in manufacturing and retail industries daily. A shoe manufacturer builds leather costs, stitching labor, and facility rent into each pair's price. A food producer allocates packaging equipment depreciation across every item produced, ensuring the final retail price covers total production expenditure and delivers a sustainable profit margin.

The disadvantages of absorption costing include its failure to account for competitor pricing strategies, which can result in uncompetitive price points. It also ignores the perceived value customers place on products, potentially pushing them toward alternatives. Because it relies on budget estimates for overhead allocation, incorrect cost figures can introduce errors across the entire pricing strategy.

Absorption costing is used by manufacturers, product-based retailers, and any business required to comply with GAAP standards for external financial reporting. The IRS also mandates it for tax purposes in the United States. Flipkart Commerce Cloud helps retailers with complex supply chains track and allocate both fixed and variable costs accurately across their full product range.

Yes, GAAP requires absorption costing for external financial reporting and inventory valuation. Under GAAP standards, businesses must include all manufacturing costs, both fixed and variable, within their product costs. This ensures financial statements accurately reflect the full cost of goods produced and held in inventory, rather than immediately expensing fixed overheads as period costs.